Valuation Methods

In general terms, there are four approaches to valuation with numerous sub-approaches within each. The first, asset-based (or accounting) valuation, is built around valuing the existing assets of a firm, with accounting

estimates of value or book value often used as a starting point. The second, market (or relative) valuation, estimates the value of an asset by looking at the pricing of 'comparable' assets relative to a common

variable like earnings, cash flows, book value or sales. The third, income approach (or, specifically, discounted cash flow valuation), relates the value of an asset to the present value of expected future cash

flows on that asset. The fourth approach, contingent claim valuation uses option pricing models to measure the value of assets that share option characteristics.

Each approach is applicable for bank valuation with several conditions.

Asset-based approach

The asset-based valuation of a bank requires valuing the loan portfolio of the bank (which comprises its assets) and subtracting the outstanding debt to estimate the value of equity. It is frequently used to establish

the liquidation value of a bank for possible legal proceedings. However, the value-based approach is difficult to apply when the bank enters multiple businesses (commercial banking, investment banking, etc.) or

regions (countries).

The necessity of the asset-based approach in bank valuation also lies in the testing of the bank’s actual book value until the valuation moment, and, consequently, it is a meaningful instrument at the negotiation (especially,

to prove the value of the bank’s intangible assets).

Market approach

The market (or relative valuation) approach is probably the simplest way to value a bank. Analysts’ conclusions based on this approach could be easily found in business reports on a regular basis, where reasonably comparable

guideline companies are defined primarily by expert opinions and multiples’ comparisons. The most sufficient multiples for bank valuation are the price-earnings ratio (P/E) and the price-to-book value ratio (P/BV).

P/E ratio, as a function of three variables – the expected growth rates in earnings, the payout ratio, and the cost of equity, depicts some specific characteristics for bank valuation revealed previously.

As

for the P/E ratio specifically, it is liable to a high volatility due to the bank policy to report a profit while creating provisions for credit losses.

Income approach

The income approach focuses on the conversion of expected future economic benefits into their present value. The discounted cash flow valuation gets the most play unacademic research and comes with the best theoretical

credentials. It is relevant to concentrate on cash flow and dividends as cash flow proxies for bank valuation.

The common free cash flow on equity (FCEE) method is highly valid for bank valuation, also because

it reflects the fact that banks can create value from the liability side of the balance sheet.

The alternative representation of FCFE is the summation of dividends paid, potential dividends, and equity repurchases and issues.

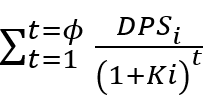

The dividend discount model (DDM) is another theoretical extension of the neoclassical discounted cash flow models, which applies to banks since they are publicly traded companies. The general form of the model is presented

by the formula:

| Value per share of equity = |

|

where DPS

i expected dividend per share in period t

K

i cost of equity.

The cost of equity for a bank has to reflect the portion of the risk in the equity that cannot be diversified away by marginal investment in the stock. Several methods are available to calculate the expected return

on equity or discount rate for banks:

- - Gordon Growth Model

- - An average profitability

- - The cost of foreign funds

- - Capital Asset Pricing Model

- - Arbitrage Pricing Theory model

The income-based approach is a well-recognized and frequently used valuation methodology, which has received wide application in practice, mostly because the bank’s value is determined by its future performance, which

is of significant concern for shareholders and other suppliers of capital.

Contingent claim valuation

Up to this point we have discussed the classical approaches to valuation.

In recent years, option pricing models (binominal, Black-Scholes-Merton, etc.), based on more advanced mathematical appliance, have been

introduced. We suppose that they might be used for bank valuation as well.

The Black-Scholes-Merton model is a function of six input factors:

- 1) the current price of the underlying stock (S)

- 2) the dividend yield of the underlying stock (R)

- 3) the option strike price (X)

- 4) the risk-free rate over the life of the option contract ( ef-Rt )

- 5) the time remaining until option expiration (t)

- 6) the price volatility of the underlying stock (σ)